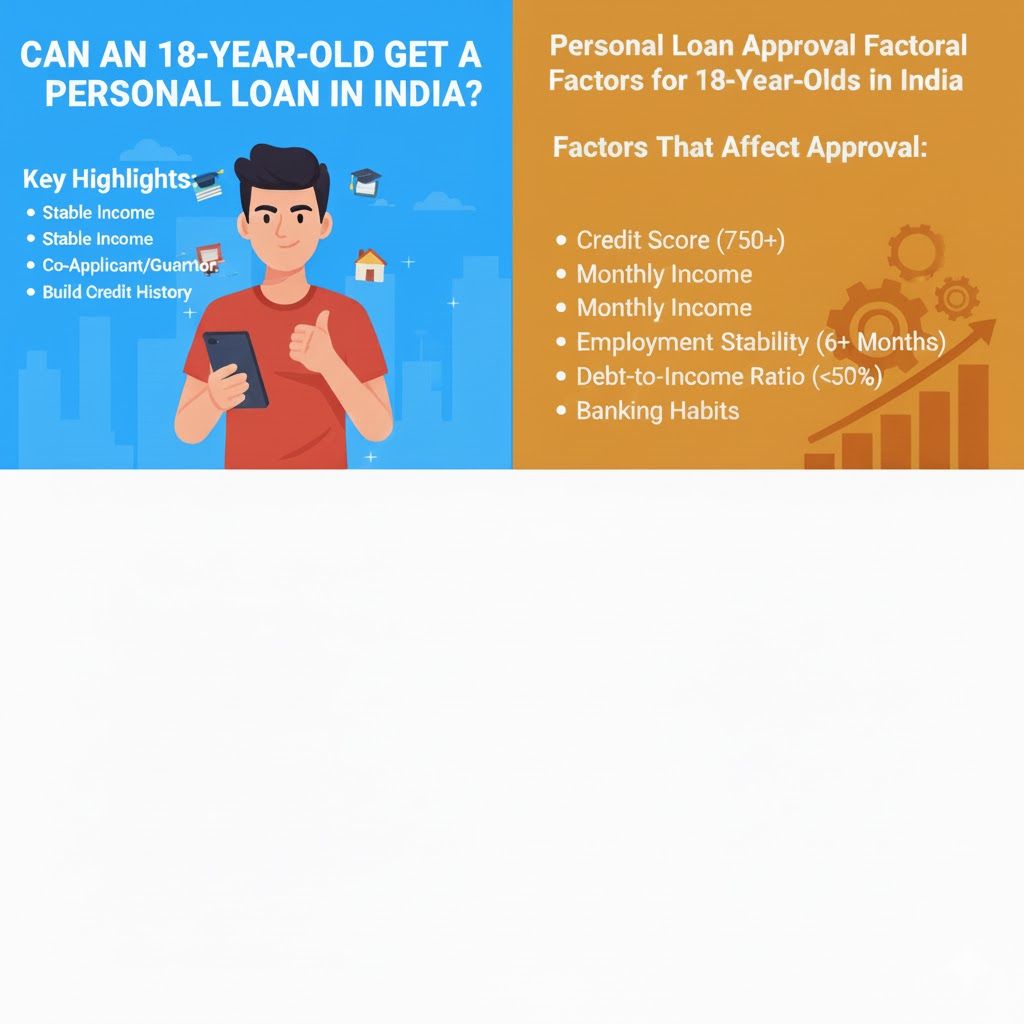

Key Highlights

It can be difficult to obtain a personal loan at the age of 18, but it is feasible if you have a reliable source of income, a co-applicant, or a guarantor with good credit.

Because they have little or no credit history, most lenders are reluctant to grant loans to 18-year-olds. Young people who work, however, might still be eligible.

Lenders evaluate applications based on a number of factors, including banking habits, debt-to-income ratio, credit score, income, and job stability.

It's thrilling to turn eighteen. You begin to take charge of your life and formally become an adult. You might occasionally need more money than you have for pocket money or a part-time job. Whether you dream of going to college, upgrading your tech, starting a small business, or dealing with an unexpected expense, you might think about getting a personal loan at 18.

But the big question is: Can an 18-year-old get a personal loan in India?

Let’s break it down simply.

What is a personal loan?

A personal loan is an unsecured loan that doesn’t require collateral. You can use it for almost anything, like education, emergencies, travel, gadgets, or personal needs.

Since there's no asset backing the loan, lenders heavily rely on:

- Income

- Credit score

- Repayment history

- Job security

This makes it tough for very young applicants, but not impossible.

Can an 18-Year-Old Get a Personal Loan?

Most 18-year-olds are either students or just starting their financial journey. At this age, many don’t have a full-time job or credit history, so lenders are cautious.

For an average 18-year-old, the situation may include:

- No income or unstable income

- No previous loan or credit card usage

- A credit score that shows “NA” (not applicable)

However, there are exceptions. Some teenagers work part-time, freelance, run online businesses, or have jobs. For these individuals, getting a personal loan is possible if they meet the right conditions.

Factors Affecting Personal Loan Approval at 18 Years

1. Credit Score

A good credit score is crucial for any personal loan. Most lenders prefer a score of 750 or above.

But what if you don’t have a score yet?

That's common at 18.

You can start building your credit profile with:

- Consumer durable loans for gadgets

- A low-limit student credit card

- A secured credit card against a fixed deposit

Making timely payments can help you build your score quickly and improve your chances for future loans.

2. Monthly Income

Your income should be regular and enough to cover your monthly payments. If your income is low or inconsistent, lenders might not approve your loan.

If that's the case, you could:

- Apply with a co-applicant, like a parent

- Choose a smaller loan amount

- Show other household income for additional support

Salary consistency matters too. If salaries are often delayed, lenders may see it as a risk.

3. Employment Stability

Most lenders prefer to see at least six months of continuous employment.

You may need to provide:

- Pay slips

- Bank statements showing monthly deposits

Working for well-established companies, like MNCs or PSUs, improves your chances of approval. Employment with newer startups or small businesses may be seen as less stable.

4. Debt-to-Income Ratio (DTI)

This ratio shows how much of your monthly income goes to paying existing loans.

A good DTI should remain below 40-50%.

If your income is ₹30,000 and your existing payments total ₹22,000, lenders will hesitate. Try to reduce your debts before applying for a new loan.

5. Loan Amount & Tenure

If your income is just adequate, consider:

- A smaller loan amount

This allows you to extend the loan tenure, which can result in lower monthly payments. Keep in mind that a longer tenure means paying more interest overall, so compare options.

6. Residential Stability

Staying at the same address for a long time shows stability. Frequently moving may create a negative impression. Living with family or in your own home adds credibility.

7. Banking & Spending Behavior

Your bank statements reveal a lot. Try to avoid:

- Overdrafts

- Impulsive spending

- Irregular withdrawals

Regular savings and a stable balance improve your financial image

Documents Needed by an 18-Year-Old

Here’s what you will need to apply for a personal loan at 18:

- Aadhaar Card

- PAN Card

- Bank statements (3-6 months)

- Salary slips or income proof if employed

- Educational documents, if applying for study funds

- Passport-size photographs

- Co-applicant documents, if applicable

Alternatives If You Are Unable to Get an 18-Year-Old Personal Loan

1. Loan from Family

This option is safe, simple, interest-free, and fast.

2. Use a Student or Low-Limit Credit Card

Pay on time to build a good credit history.

3. Apply for Scholarships or Grants

If your expenses are education-related, look into government and private scholarships.

4. Crowdfunding

This can be useful for medical needs, emergencies, or creative projects where friends and the community can contribute.

In conclusion,

Getting a personal loan at the age of 18 is not impossible, but it can be challenging. Lenders might take your application into consideration if you're making money, keeping your finances steady, and handling your money well.

There are alternative ways to meet your financial needs and begin establishing your credit profile early, even if you encounter difficulties. Start small, cultivate sound financial practices, and get ready for future opportunities. You are just starting your journey at the age of 18, and every wise choice you make now will strengthen your future tomorrow.

Ready to compare real offers?

One application. 10+ RBI-registered lenders. Free for borrowers.