Why Is Your Interest Rate on a Personal Loan Higher than Expected and How To Lower It

Personal loans are a very useful way of borrowing money for a range of urgent needs, including medical emergencies, renovations, traveling, or even to consolidate debts. However, many borrowers are shocked to discover what their interest rates are when applying to lenders for personal loans. Many times, the interest rates offered to borrowers are much higher than what they anticipated.

When borrowers understand why lenders charge such high-interest rates and some of the factors involved in determining the rates, they may be able to negotiate a better interest rate through their lender. This article will discuss some of the reasons for high-interest rates and offer some suggestions for reducing those interest rates.

Unlike a mortgage on a house or a car, personal loans are unsecured loans. This means there is no property or equipment used to secure the loan with the bank (lender). Without collateral, there is higher risk to the lenders. Therefore, in general, lenders charge higher interest rates for unsecured loans than they do for secured loans.

The above factor is one reason lenders will charge you a higher-interest rate (than what you may have expected) for your personal loan; however, additional factors are involved in what interest rate you may qualify for with a personal loan.

How come Personal Loan Rates Are so High?

Unlike mortgages or auto loans, personal loans are unsecured loans. This means that lenders don't take into account the value of your home or car as collateral. The level of risk to the lender is greater without recourse to securing a loan with an asset, leading lenders to charge higher interest rates for unsecured loans.

There are also additional influences that impact the rate you receive for a personal loan.

1. Low Credit Score

Your credit score is one of the most critical criteria considered by lenders when deciding whether to approve your application for a personal loan.

A low credit score indicates to lenders that you present a higher degree of risk.

Lenders typically offer a borrower with a poor repayment history with a higher rate of interest and a person with a strong repayment history with a lower rate of interest.

Your credit score may be impacted negatively if other loans you have are paid late, you default on other loans, or carry more credit card debt than you can manage.

Generally, a person will have an easier time qualifying for low-interest loans when they have a credit score of a minimum of 750.

2. High Debt Load

If you already have a number of loan balances or a number of credit card balances, the lender will view you as financially overextended.

Lenders are concerned about the following key factors related to your debt:

Debt-to-income ratio

Obligation to pay monthly loan/credit card payments (EMI)

Ability to take on additional debt

When you have a large debt load, the lender perceives this as greater risk, which will drive the interest rate on your loan high

3. Income or Employment Stability

Most lenders look favorably on an applicant who has steady income as well as stable employment.

The interest rates may be affected if:

You frequently change jobs

You regularly receive fluctuating or inconsistent income

You work in a risky employment field.

Lenders tend to offer better loan terms to someone who has been consistently employed with a stable income.

4. Short Credit History

If you're new to credit with limited prior borrowing experience, lenders can only review a small amount of information regarding your prior repayment history.

This is considered a “thin credit file”.

Due to the uncertainty of your repayment record, lenders may choose to charge significantly higher interest rates to protect themselves against this risk.

5. Loan Size and Term (Tenure)

Both loan size and the length of time (purchase order or term) over which to repay the loan affect interest rates.

As examples:

Longer-term loans may have higher rates;

Smaller loans often have higher rates;

Larger loans without sound financial backing increase lender risk.

Ideal loan size and term combinations will decrease the cost of borrowing.

How to Lower Your Personal Loan Interest Rate

Here are the ways that you can secure a lower interest rate for your personal loan:

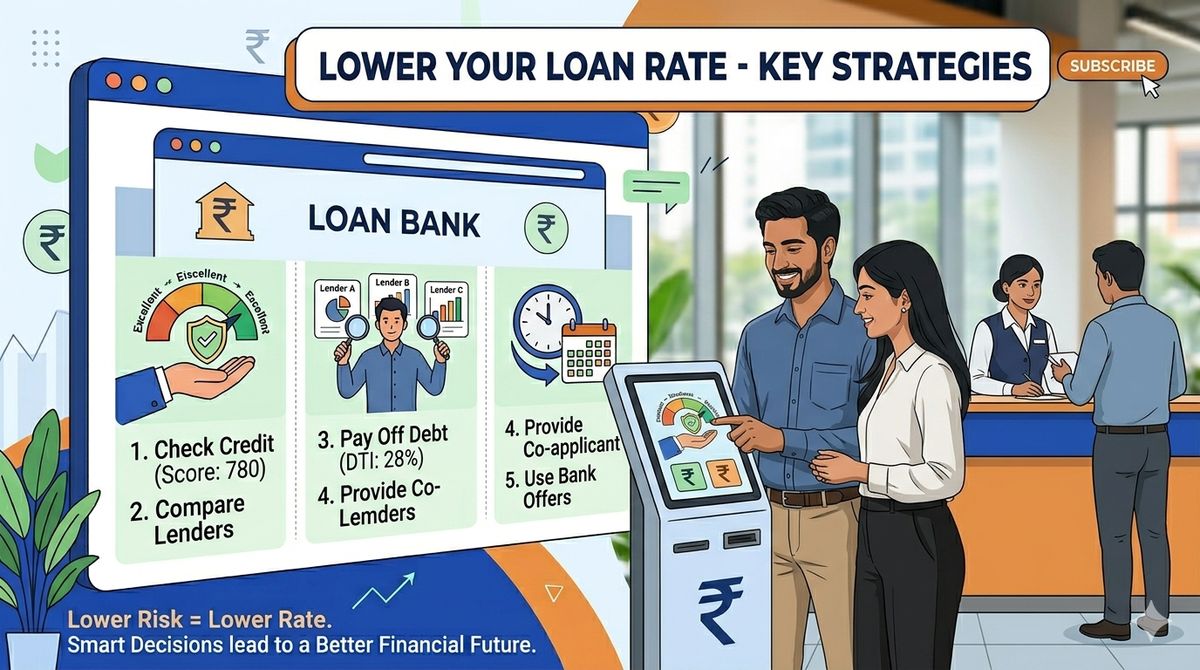

1. Make Sure You Have a Good Credit Score

You should try to make sure your credit is in a good place before you apply. for example:

Pay your credit card bill in full and on time

Don’t default on any loan

Keep your overall credit utilization below 30%

Check your credit report to make sure there are no errors

When the creditor sees that you are responsible with your credit, you are likely to get a better interest rate.

2. Get Quotations from Different Lenders

Whenever you apply for a loan, different creditors offer different interest rates depending on their policies and risk assessment models.

So when deciding whom to apply to for your loan, always compare loan offers. make sure you compare all the loan terms and conditions such as: the processing fees, hidden costs, and the total cost of borrowing the money.

Even a small difference in interest rates can save you thousands over the life of the loan.

3. Select a Shorter Loan Term

One of the benefits of selecting a shorter loan term is you generally have a lower interest rate. although your monthly payment amounts will generally be higher, over time you are saving a lot in interest.

Some benefits of a shorter loan term are: you will have a lower total interest amount to pay, your loan will be paid off quicker, and you will tend to have better financial discipline between the two payments.

You want to find a balance between payment affordability and total interest savings.

4. Applying with a Co-Applicant

By adding a financially sound co-applicant to your application, you may decrease your perceived risk to a lender.

A co-applicant's good credit rating, stable income, and strong financial position can increase the likelihood of being granted a loan and result in a lower interest rate for you.

5. Strengthen Your Relationship With Your Bank

You may receive more favourable loan offers as an existing customer.

If you maintain:

A Salary Account

Fixed Deposits

A Good Transaction History

you may qualify for better interest rates than new customers.

Key Factor | Impact on Rate | How to Lower Your Rate |

Credit Score | High Score = Lower Rate | Pay bills on time; keep utilization < 30%. |

Debt Load | Low Debt = Lower Rate | Reduce existing balances before applying. |

Income Stability | Steady Job = Lower Rate | Provide proof of consistent, long-term income. |

Loan Term | Shorter Term = Lower Rate | Choose a shorter tenure to save on total interest. |

Credit History | Long History = Lower Rate | Avoid closing old accounts; build a track record. |

Application Type | Co-applicant = Lower Rate | Apply with a partner who has a strong credit score. |

Bank Loyalty | Existing User = Lower Rate | Check with your primary bank for loyalty offers. |

Conclusion

There are many factors that have an impact on personal loan interest rates; credit reports, credit scores, steady income levels, the amount of debt currently held, and credit repaying history among them.

Higher interest rates should not be seen solely as a barrier to receiving a loan; understanding the reasons how and why higher rates exist may also provide opportunities to proactively have a better chance at securing lower rates.

If you want to have the lowest possible borrowing costs associated with borrowing money, developing and continuing to maintain an all-around good credit rating will be the best way to do. Comparing lenders, selecting an appropriate loan term, and working to minimize total liability from now until willing to make payments on your loan will all contribute to reducing the amount of money you will ultimately spend, relative to what it will cost to borrow funds.

Before deciding to apply for a personal loan, you want to know where you currently stand financially, then choose the right lender based upon having both transparent loan options as well as competitively priced loans.

Making good financial choices today will help gain you a much more secure financial future.

Ready to compare real offers?

One application. 10+ RBI-registered lenders. Free for borrowers.